Our Blogs

Explore articles, tips, and strategies to help you make confident money decisions at every stage of life.

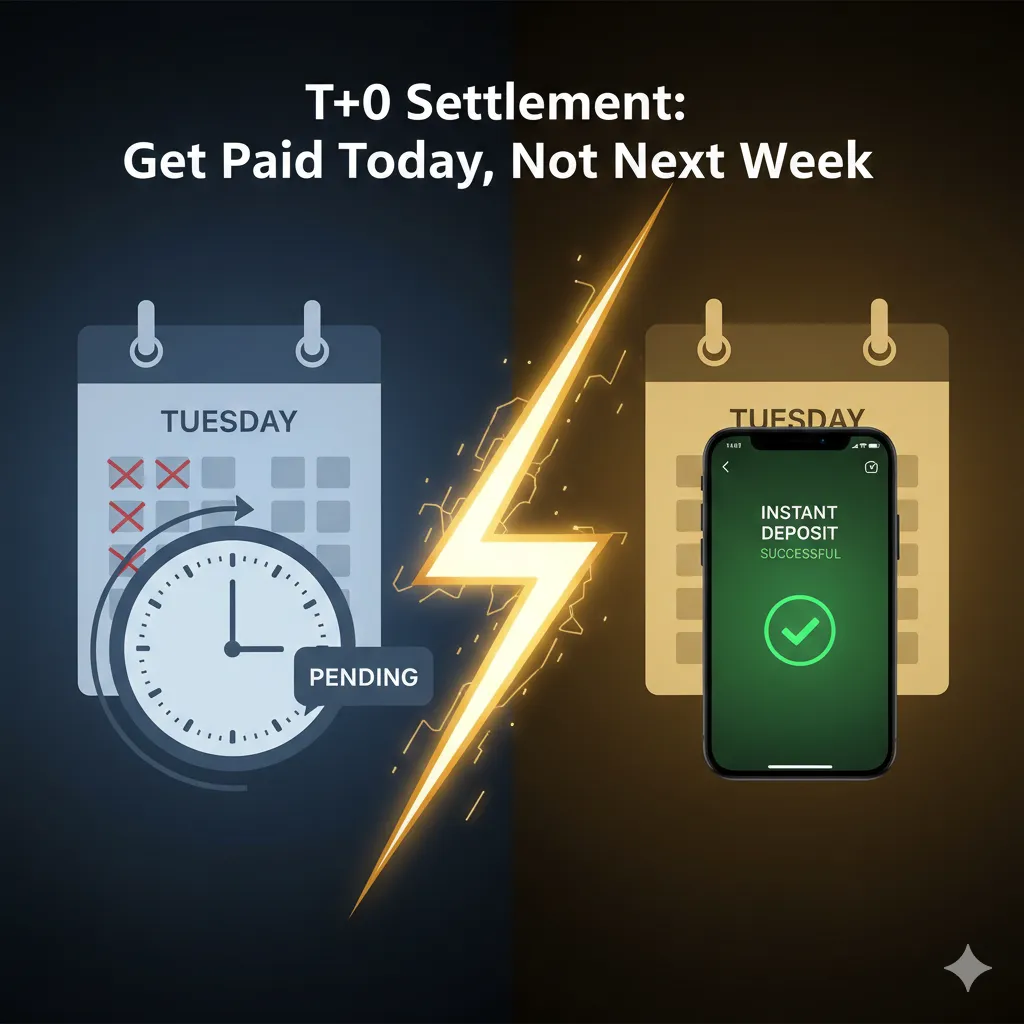

T+0 Settlement: Why 3-Day Funding Is Outdated | Circle Processing

In the early days of my career in the payment industry, "T+3" was the gold standard. You made a sale on a Monday, the bank moved some digital papers around, and by Thursday, if you were lucky and there wasn't a bank holiday, you finally saw that money in your account. Back then, the world moved a little slower. Your suppliers gave you thirty days to pay, and your rent wasn't due until the first of the month.

Fast forward to 2026, and that three-day delay is no longer just a minor inconvenience, it is a threat to your business. In a city like New York, where inventory costs are fluctuating by the hour, and your staff expects their digital tips to be available instantly, a settlement delay is a bottleneck that can choke your growth.

At Circle Processing, I’ve made it my mission to kill the "waiting period." We believe in T+0 settlement—the idea that if you do the work today, you should get paid today.

The Cash Flow Gap: The Silent Business Killer

The biggest pain point I hear from Long Island retailers and Jersey City restaurateurs is the "Cash Flow Gap." You have a record-breaking Saturday night. Your POS shows $15,000 in sales. You feel like a success. But on Sunday morning, when you need to place a $5,000 produce order or fix a broken refrigerator, your bank balance says you're broke.

That "paper profit" doesn't pay the bills. When your capital is trapped in the "pending" ether of the banking system, you are essentially giving a three-day interest-free loan to the big banks. Meanwhile, you’re potentially missing out on bulk-buy discounts from your suppliers or, worse, having to use a high-interest credit card to cover a temporary shortfall. Cash flow management isn't about how much you make; it’s about when you can access it.

What is T+0 Settlement (And Why Do You Need It)?

In the technical world, "T" stands for Transaction Date. Most processors still operate on T+1 or T+2. T+0 means the settlement happens on the same day the transaction occurs.

By utilizing modern same-day funding rails like the RTP (Real-Time Payments) network or FedNow, we can bypass the archaic batch-processing cycles of the old ACH system. Instead of your money sitting in a holding tank, it moves directly into your operating account.

For a small business, this is a game-changer. It means your "End of Day" truly means the end of the financial cycle. You can reconcile your books at 10 PM and see the funds ready for your 6 AM supply run.

Instant Payouts NY: Weekend and Holiday Freedom

The old banking system only works on "business days." If you have a massive weekend at a street fair or a holiday rush, you could be waiting until Tuesday or Wednesday to see a dime of that revenue.

True instant payouts, NY providers (like us) don't care about the calendar. If you process a transaction on a Sunday afternoon, you can trigger a payout that hits your account in minutes. This "24/7/365" liquidity is what allows modern businesses to stay agile. You can pay your casual staff as they finish their shifts or jump on a limited-time inventory deal that would be gone by the time a Tuesday settlement arrives.

FAQs

What is the difference between T+0 and same-day funding?

T+0 settlement technically means the trade or transaction settles on the same day it occurred. Same-day funding is the service provided by processors to ensure that the net funds from your daily sales are deposited into your bank account before the close of that same business day, rather than waiting for the following day or later.

Are there extra fees for instant payouts for my business?

Most providers charge a small percentage fee (typically between 1% and 1.5%) for the convenience of an instant payout outside of the standard settlement cycle. However, many businesses find that the cost of the fee is far lower than the "cost" of being unable to restock inventory or having to use expensive short-term credit.

Does my bank need to support real-time payments for me to get T+0 settlement?

To receive funds within seconds or minutes, your receiving bank must be part of a real-time payment network like RTP or FedNow. If your bank does not support these, you can still often get "Same-Day ACH," which delivers funds within a few hours during the business day, but not instantly on weekends.

Can all types of transactions be settled the same day?

Most standard credit and debit card transactions are eligible for same-day funding. However, very large transactions (often over $100,000 or $1,000,000, depending on the provider) or transactions flagged for fraud review may still be subject to standard settlement times.

How does same-day funding improve my business credit?

By having immediate access to your revenue, you are less likely to miss vendor payments or carry high balances on business credit cards. Consistently paying your bills on time and maintaining a healthy cash balance is one of the fastest ways to improve your overall business credit profile.

Reclaim Your Friday Night Revenue

You worked hard for that money today. There is no reason a bank should be holding onto it for the next seventy-two hours.

Would you like me to look at your current processing agreement and show you how we can move you from a "waiting" cycle to a "winning" cycle with a T+0 settlement plan that keeps your cash where it belongs—in your account?

Why Circle Processing?

Frequently Asked Questions

Clear answers to help you make confident financial decisions.

Q: What is the main difference between Dual Pricing, Cash Discount, and Surcharging?

The main difference is how the price is presented to the customer. Dual Pricing shows two prices upfront (e.g., $10 cash / $10.40 card). A Cash Discount shows one higher price and automatically applies a discount if the customer pays with cash. Surcharging shows one price and adds a fee at the end only for credit card transactions. Our experts can help you choose the best fit for your business.

Q: Are these fee-elimination programs legal?

Yes. Cash Discount and Dual Pricing programs are legal in all 50 states when implemented correctly with transparent signage, which we provide. Credit card surcharging is also legal in most states, but is prohibited in a few, such as Connecticut and Massachusetts. We are compliance experts and will ensure your business always operates within the rules.

Q: Which Clover device is right for my business?

It depends on your needs. The Clover Station Duo is perfect for high-volume countertops with its dual screens. The Clover Flex is a powerful handheld device ideal for restaurants and mobile payments. The Clover Mini is a compact, all-in-one solution for smaller spaces. We can help you select the perfect hardware during your free consultation.

Q: What makes Circle Processing different from other Clover resellers?

Our focus is on being your profitability partner, not just a hardware vendor. Our core expertise is in the complex, compliant implementation of fee-elimination programs. We combine that with transparent pricing, no long-term contracts, and dedicated, 24/7 U.S.-based support to help your business thrive.

Get Started

Want to work with us?

Let’s create a personalized financial plan that puts your goals within reach — starting today.

COMPANY

LEGAL

SOCIALS

Copyright 2026. Circle Processing. All Rights Reserved.