Merchant Statement Audit: How to Spot & Cut Junk Fees | Circle Processing

I’ve sat across the desk from hundreds of business owners in the Tri-State area, from local diners in Hoboken to boutique retailers in Cherry Hill. Usually, the conversation starts with a sigh of frustration. They hand me a six-page document filled with tiny fonts, cryptic acronyms, and a "Total Amount Due" that seems much higher than the "Low Rate" they were promised.

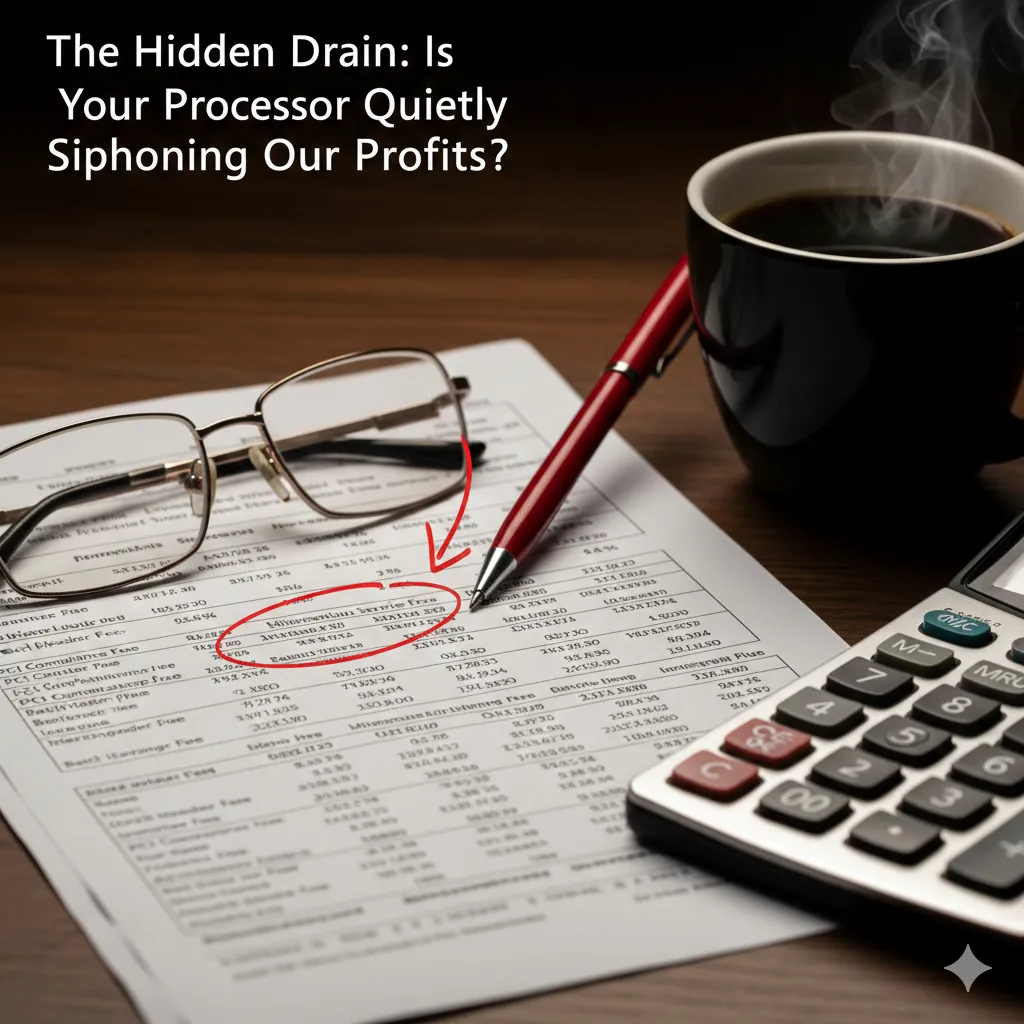

Most business owners treat their merchant statements like a utility bill, they glance at the total, assume it's the cost of doing business, and pay it. But in my years at Circle Processing, I’ve learned that these statements are often designed to be confusing. If you can't read it, you can't challenge it.

There is a "hidden drain" in almost every legacy processing agreement. These are the junk fees, small, recurring charges that don't help you process a single dime but add up to thousands of dollars in lost revenue over the year. It’s time to pull back the curtain and bring some transparency in finance back to your desk.

The "Anatomy" of a Junk Fee

When I perform a merchant statement audit, the first thing I look for are the fees that have nothing to do with "Interchange" (the actual cost from the banks). If you see these on your bill, you are likely being overcharged:

Statement Fees: In 2026, charging $10 or $15 a month to "generate" a digital PDF is a relic of the past. Many legacy providers still tack this on simply because they know most people won't notice a small ten-dollar charge.

PCI Non-Compliance Fees: This is the most common "gotcha" fee. I’ve seen businesses paying $30, $50, or even $100 a month because they haven't filled out a simple 15-minute annual survey. Processors often won't remind you to do it because they make more money when you stay non-compliant.

Regulatory Product Fees: Sometimes labeled as "Efficiency Fees" or "Service Fees," these are often just pure margin for the processor disguised as government requirements.

Why "Teaser Rates" Are the Ultimate Distraction?

Many businesses in payment processing NJ markets are lured in by a "Qualified Rate" of 1.5%. It sounds great on a sales flyer. However, when you actually look at the statement, you realize that almost none of your transactions are "Qualified."

Reward cards, business cards, and even standard "dipped" transactions get "downgraded" into mid-qualified or non-qualified tiers. This tiered pricing model is the perfect hiding spot for markups. While the salesperson talked about 1.5%, your "Effective Rate" (total fees divided by total sales) is likely closer to 3.5% or 4%.

How to Conduct Your Own 10-Minute Audit?

You don't need to be an accountant to spot the leaks. Grab your last three months of statements and follow this simple process:

Calculate the Effective Rate: Take the "Total Fees Charged" and divide it by the "Total Volume Processed." If you processed $10,000 and paid $400 in fees, your rate is 4%. For most retail or restaurant businesses, anything over 2.5% is a sign that junk fees are present.

Scan the "Fixed" Section: Look for any fee that stays exactly the same every month. Statement fees, monthly minimums, and "support" fees are all negotiable or, in many cases, completely unnecessary.

Check the Compliance Line: Search for "PCI" or "Non-Val" (Non-Validation). If there is a charge there, you are literally throwing money away for a survey you could complete in your lunch break.

At Circle Processing, we believe that transparency in finance isn't just a buzzword, it's a requirement for a healthy partnership. We don't believe in "teaser" rates that disappear after ninety days, and we certainly don't believe in charging you for the "privilege" of receiving a bill.

FAQs

What is a PCI non-compliance fee, and why am I paying it?

A PCI non-compliance fee is a penalty charged by your processor when you haven't completed your annual Self-Assessment Questionnaire (SAQ). This fee is intended to "encourage" security, but many processors use it as a silent profit center. You can usually stop this fee immediately by completing the compliance survey through your processor's portal.

What is the "Effective Rate" on a merchant statement?

The effective rate is the only number that truly matters. You calculate it by dividing your total monthly fees by your total monthly processing volume. This bypasses the confusing "teaser rates" and shows you the actual percentage of every dollar you are losing to processing costs.

Why are my merchant processing fees higher than the rate I was quoted?

Most quotes focus on "Qualified" rates, which only apply to basic debit cards. Most modern transactions involve rewards, business, or international cards, which "downgrade" to higher tiers. Additionally, fixed monthly junk fees and PCI penalties can significantly inflate your actual cost above the quoted rate.

How often should I perform a merchant statement audit?

You should review your statement every month, but a deep audit should be performed at least once a year or whenever you notice your effective rate creeping upward. Processors often introduce new "program fees" or "regulatory adjustments" quietly at the start of a new quarter.

Can I negotiate the fees on my merchant statement?

Yes, many "processor markup" fees and monthly service charges are negotiable. However, the interchange and assessment fees set by the card networks (Visa/Mastercard) are fixed. A transparent provider will clearly separate these non-negotiable costs from their own markup.

Reclaim Your Revenue

Every dollar spent on a "junk fee" is a dollar that could have been reinvested in your staff, your marketing, or your local community.

Would you like me to take a look at your most recent statement? I can perform a line-by-line audit for you and show you exactly where the "hidden drain" is located, with no obligation to switch.